Sequence of returns risk refers to the possibility that people who experience a stock market downturn in the first three to five years of retirement may deplete their savings prematurely if they take withdrawals from their portfolios while the market is going down.

What does this mean? Let’s look at some examples.

Remember, most financial advisors out there are still telling their clients that when they retire, the extent of their “retirement plan” should be to start withdrawing 4% of their retirement portfolio annually to cover their monthly living expenses. However, even if they recommend a more conservative 3% or 2%, they still haven’t created an actual plan for their client’s retirement that protects principal.

This kind of retirement “advice” can jeopardize your retirement. Why? Here is a hypothetical example to illustrate exactly how sequence of returns risk works.

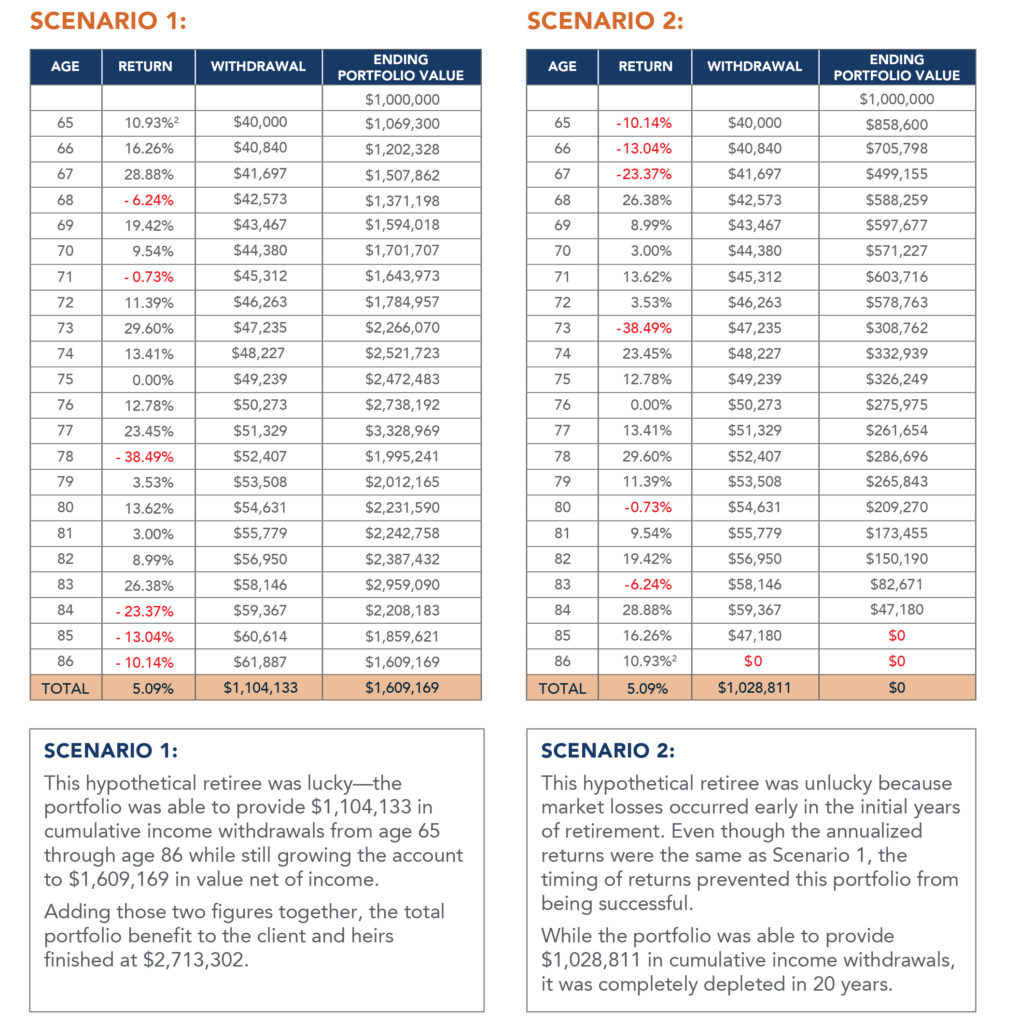

In the tables below, on the left, Scenario 1 shows the actual S&P average stock market returns for 20 years (years 2000 – 2021). On the right, Scenario 2 shows those exact same returns—in reverse (years 2021 – 2000). Their average rate of return is exactly the same.

In both scenarios, the retiree is 65 years old and retires with $1 million:

In both scenarios, the retirees withdraw the exact same amount of money each year–4% per year plus a 2.1% annual increase for inflation each year through age 86.

Notice that the Scenario 2 retiree runs out of money at age 85, while the Scenario 1 retiree still has more money in their portfolio than when they retired!

Yet, the average return rate was exactly the same for both at 5.09%, and the annual withdrawal amounts were the same. The yearly stock market average return percentages were also exactly the same, except they were in reverse order.

In fact, the only difference was that the stock market was dropping for the first three years of Scenario 2’s retirement—and that is what sequence of returns risk means. With sequence of returns risk, the timing of returns can affect portfolio income success.

No one has a crystal ball to know what’s going to happen to the stock market when you retire, so how can you protect yourself?

The Fixed Indexed Annuity

An often-overlooked asset class for retirement is the guaranteed* income provided by a fixed indexed annuity. Fixed Indexed Annuities (FIAs) and riders can address many different retirement risks, including sequence of returns.

If you are not reliant on withdrawing money from the stock market to cover your basic living expenses, then you will not be subject to sequence of returns risk. By making sure a combination of your Social Security plus an FIA will cover your monthly expenses, you can avoid the necessity of withdrawing money from your portfolio when markets are down. You can simply withdraw funds when markets are going up or holding steady to cover your extras like trips or fun money.

Even if you do withdraw some money from your portfolio along with receiving some income from a fixed indexed annuity, you can protect yourself.

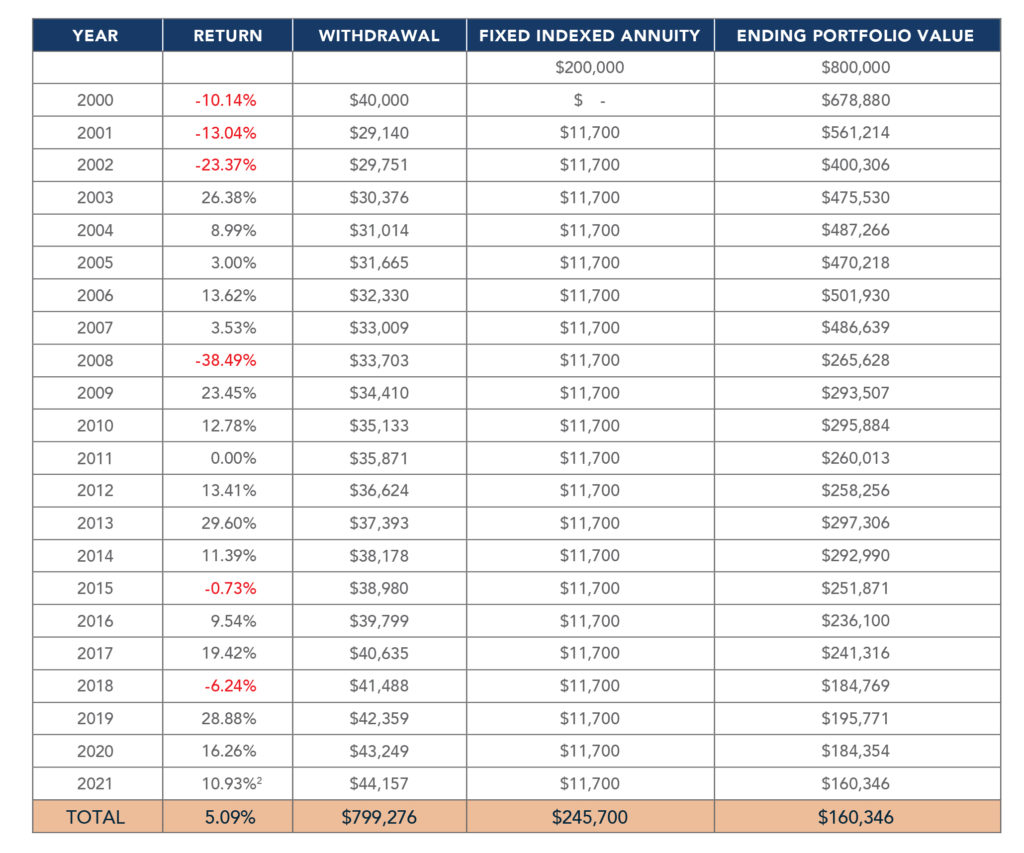

Here is an example of how using an annuity can help even if you withdraw money from the market during a downturn. Below is our same Scenario 2 retiree, who used 20% of his $1,000,000 retirement nest egg and purchased a fixed indexed annuity with guaranteed* lifetime income which paid him $11,700 per year.

By age 86, this retiree had received a total of $1,044,976 (adding up withdrawals plus the annuity payments), yet he still had $160,346 remaining in his portfolio. And this example does not include the potential growth of the annuity which could result from interest-crediting.

By age 86, this retiree had received a total of $1,044,976 (adding up withdrawals plus the annuity payments), yet he still had $160,346 remaining in his portfolio. And this example does not include the potential growth of the annuity which could result from interest-crediting.

Your retirement plan could look even better.

Don’t retire before working with a qualified financial advisor to run all of your actual numbers and help you create a personalized retirement plan based on your unique situation and goals.

Call Alpha Beta Gamma Risk Management at (866) 837-0999 for a no-obligation conversation about your retirement plan.

*Guarantees and protections of fixed indexed annuities are subject to the claims-paying ability of the issuing insurance company. Fixed indexed annuities are contracts purchased from a life insurance company. They are designed for long-term retirement goals, and also intended for someone with sufficient cash and liquid assets for living expenses and unexpected financial emergencies, including, for example, medical expenses. Depending on the product, fixed indexed annuities may include surrender charges, rider charges and other fees.

A fixed indexed annuity is not a registered security or stock market investment. As such, it does not directly participate in any stock, equity or bond investments, or index. Gains on indexed accounts are based on participation rates and other conditions offered by the issuing insurance company. If purchased with tax-deferred money, withdrawals are subject to income tax, and as with all pre-tax qualified retirement money, withdrawals before age 59½ may be subject to taxes plus a 10% early withdrawal federal tax penalty.

This website is for informational purposes only and is not intended to provide any recommendations or tax or legal advice.