There is a lot of debate about the 4% withdrawal rate in retirement. Some believe that the markets will continue to perform adequately for retirees, allowing them a withdrawal rate of 4% a year adjusted for inflation while safely ensuring they never run out of money.

But some leading economists and financial planners argue that the 4% rule can no longer be used and that the withdrawal percentage should be considerably lower.

With interest rates at 300-year lows and the 10-year US Treasury note at 1.28%1, the traditional conservative fixed-income, bond-heavy retirement portfolio has been abandoned in favor of seeking extra yield and growth, often taking on additional risk in the overall portfolio in the form of dividend stocks and/or high-yield bonds.

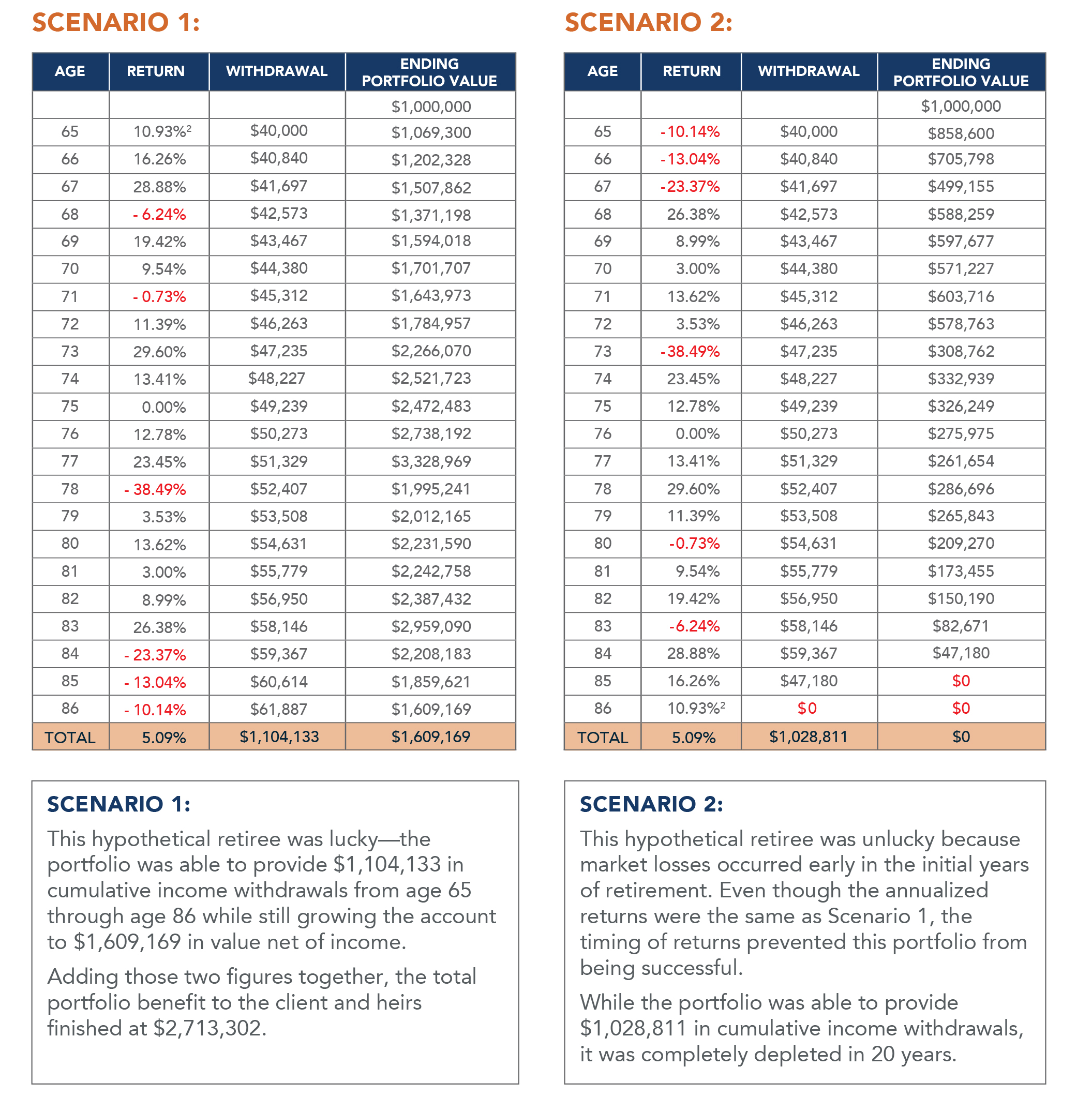

In order to illustrate the potential negative impact of sequence of returns during the important first five years immediately following retirement, we have compared some hypothetical scenarios based on stock market history.

SEQUENCE OF RETURNS RISK IS ALL ABOUT TIMING

Two Scenarios with Exactly the Same Returns—In Reverse Order

• In both scenarios, the retiree is 65 years old and retires with $1 million.

• In both scenarios, the retiree withdraws 4% per year plus a 2.1% annual increase for inflation each year through age 86.

• Scenario 2 shows the actual S&P average stock market returns from the years 2000 – 20212. Scenario 1 simply inverts and reverses those same returns, starting with the 2021 S&P average.

This is what is meant by sequence of returns risk: the timing of returns can affect portfolio income success.

GUARANTEED INCOME STRATEGY:

Fixed Indexed Annuities

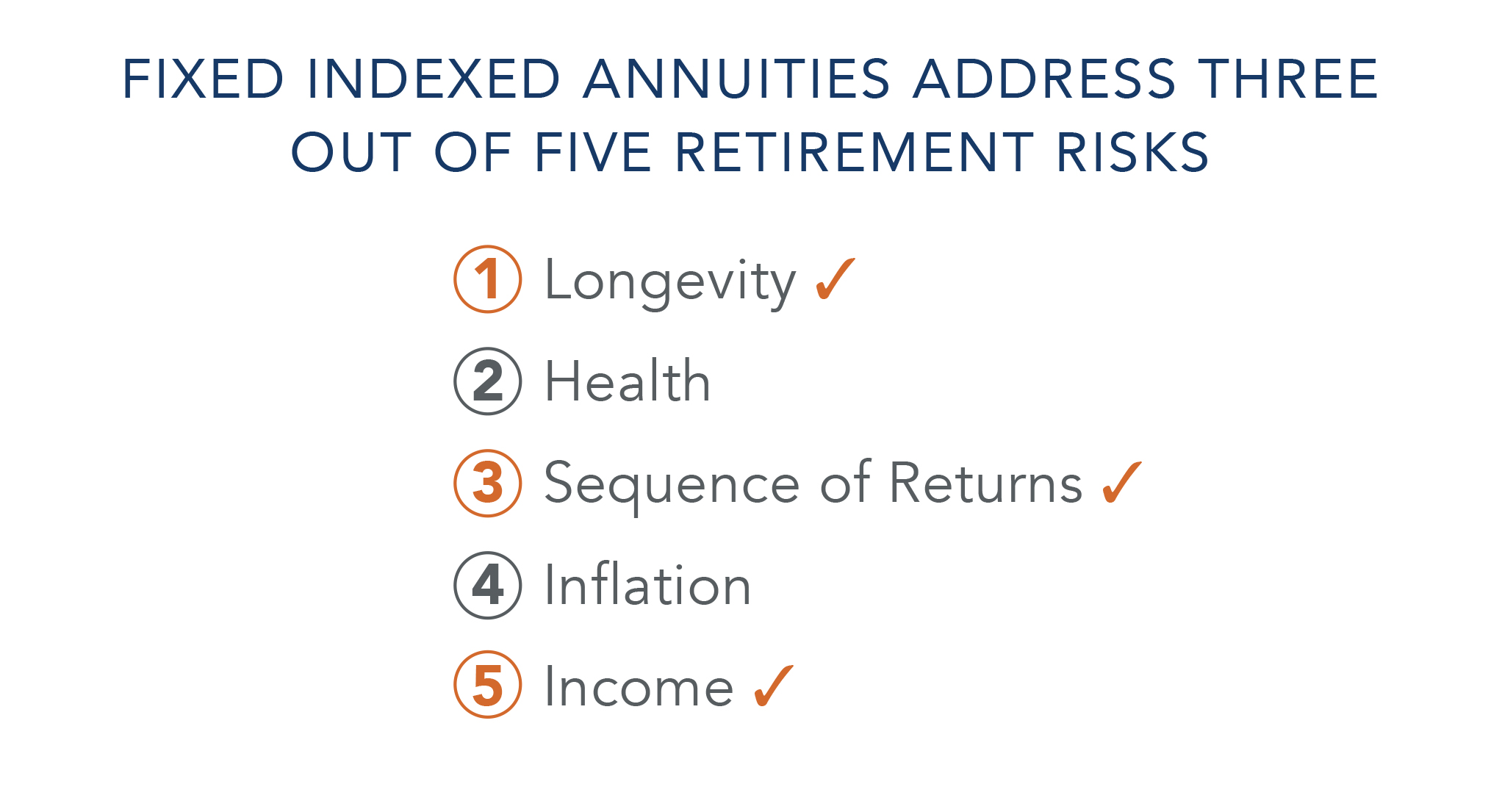

An often-overlooked asset class for retirement is the guaranteed income provided by a fixed indexed annuity. Fixed Indexed Annuities (FIAs) and riders can address many different retirement risks, including sequence of returns.

In fact, the only asset class that can help mitigate three of the five risks in retirement—longevity, sequence of returns and income—is an annuity with guaranteed income.

A Fixed Indexed Annuity (FIA) with an optional Guaranteed Income Rider* provides guaranteed lifetime income that may help offset portfolio sequence of returns risk. Guaranteed income lessens the reliance on the portfolio to generate income, helping mitigate the risk of negative timing of returns and providing security to cover income needs.

Having guaranteed income gives the retiree the option to leave money in the portfolio during market downturns rather than being forced to take withdrawals for living expenses which can hasten a portfolio’s decline.

HOW GUARANTEED INCOME CAN MITIGATE SEQUENCE OF RETURNS RISK

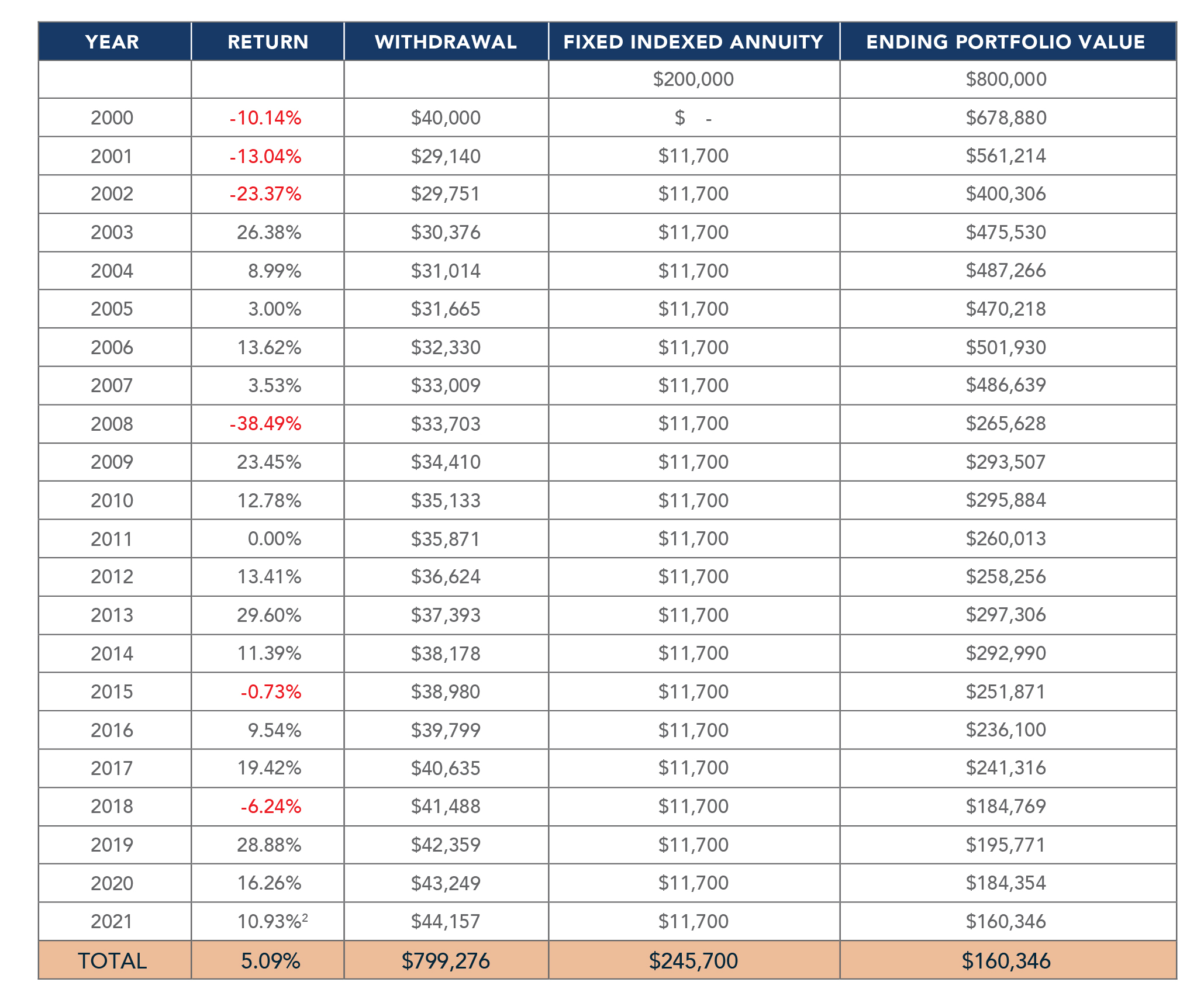

Scenario 2 Option, Adding an FIA

SCENARIO 2 OPTION:

The hypothetical 65-year-old retiree with $1 million saved who experienced market downturns early in retirement could have avoided running out of money by using a guaranteed income fixed indexed annuity (FIA).

If the retiree had allocated 20% of the portfolio into a fixed indexed annuity with guaranteed income, the FIA could generate $11,700 in guaranteed income annually and $245,700 in total as shown, assuming a 65-year-old male owns the FIA contract and income is deferred for one year.

In this scenario, the portfolio was able to provide $1,044,976 in cumulative income withdrawals while still maintaining a $160,346 portfolio balance.

NOTE: This result does not include a potential increase in the fixed indexed annuity due to interest-crediting.

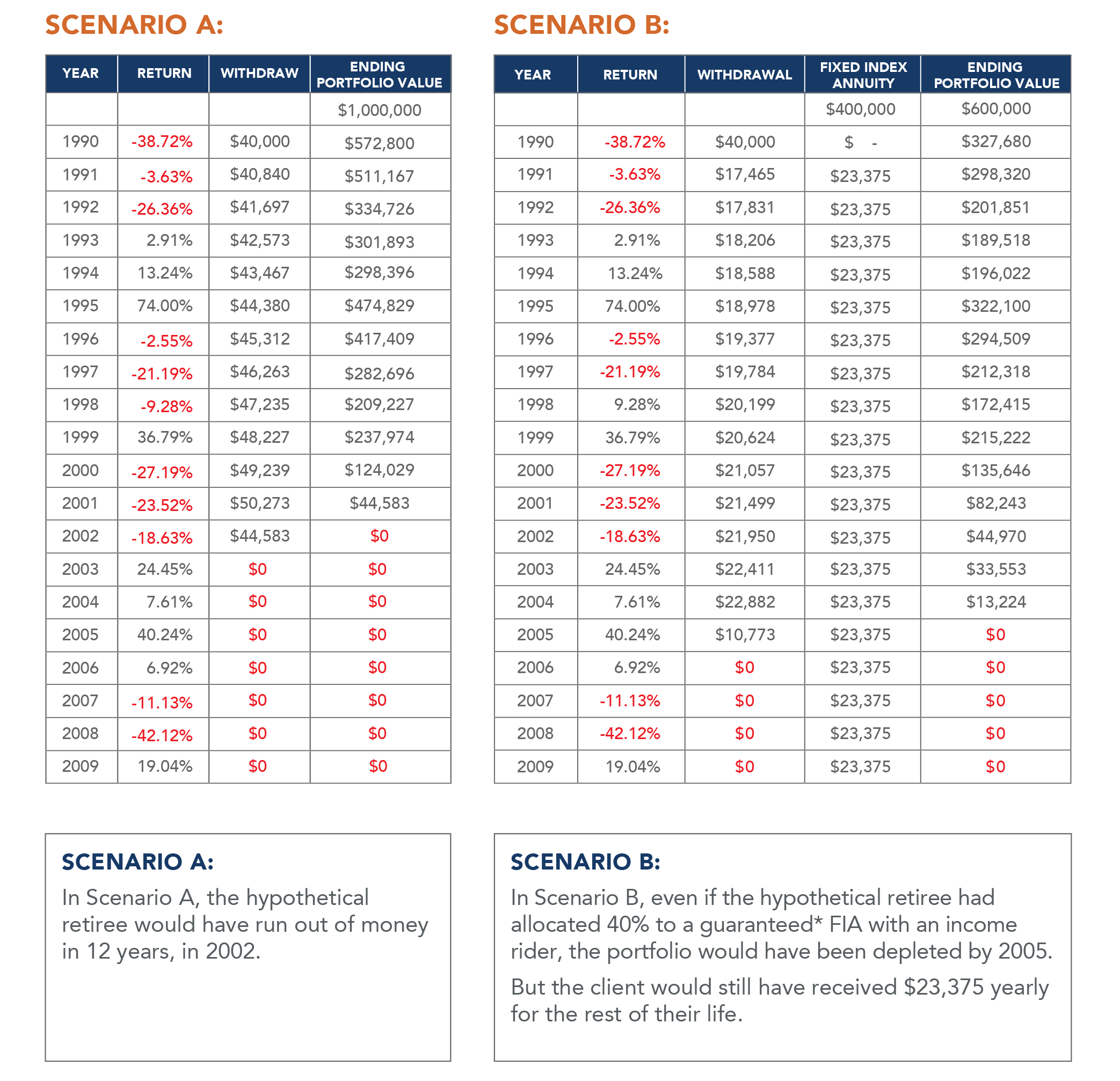

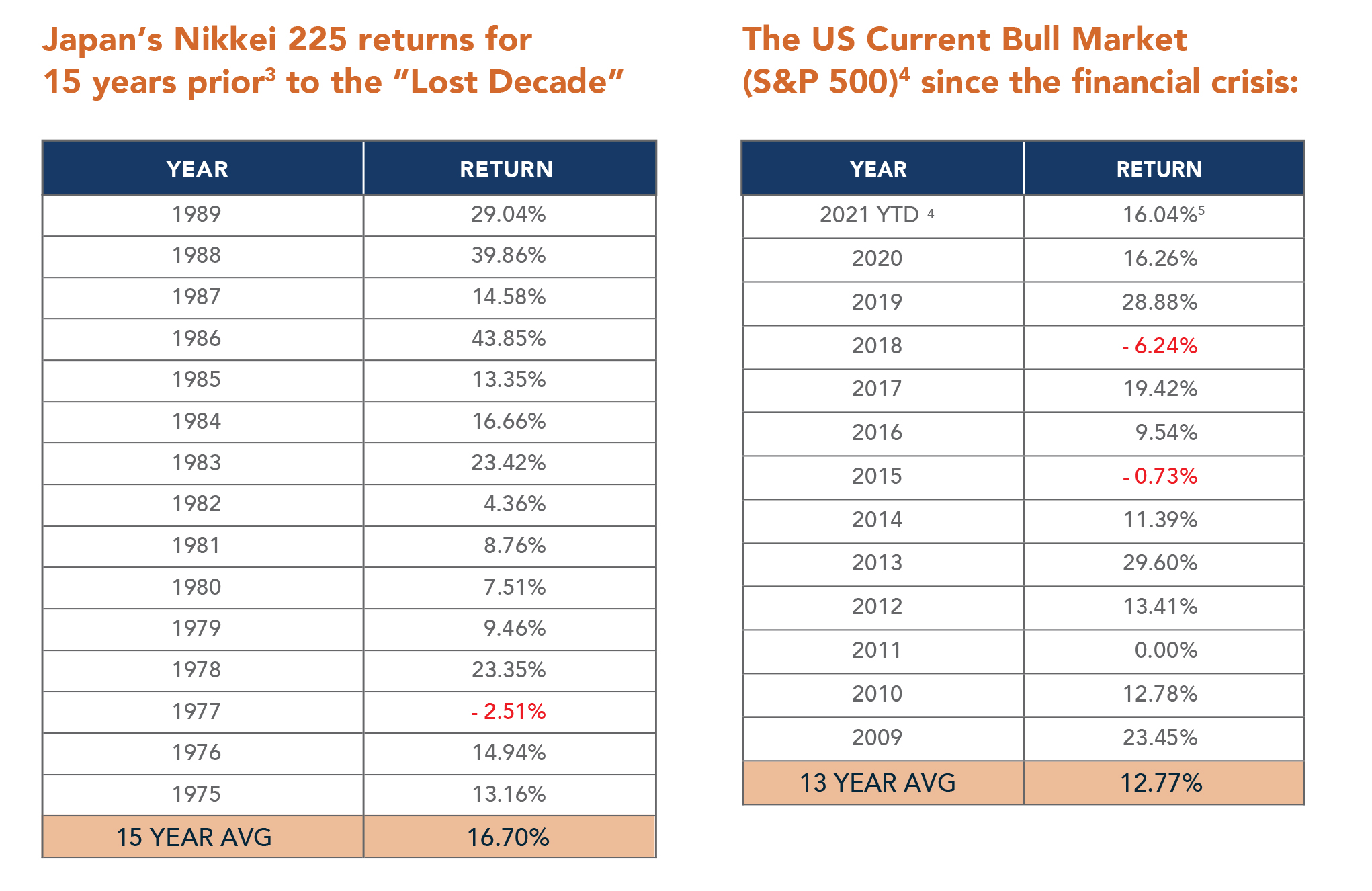

A LOOK BACK AT JAPAN’S “LOST DECADE”

• These charts illustrate the Nikkei 225 index losses during Japan’s “Lost Decade” from 1991 – 2001. Per Investopedia, rising interest rates set a liquidity trap at the same time a credit crunch was unfolding.3

• In both of the illustrated scenarios above, the retiree is 65 years old and retires in 1990 with $1 million invested in the Nikkei 225 Index.

• In both scenarios, the retiree withdraws 4% per year plus a 2.1% annual increase for inflation.

• Scenario B includes an FIA with guaranteed income.

COULD HISTORY REPEAT ITSELF?

While history may not repeat, there is a saying that “it often rhymes.” While the United States may not experience a lost decade like Japan, it is something to consider and plan for. As the U.S. is potentially in the late innings of its current bull market run, it just makes sense to hedge against multiple retirement risks in the retirement portfolio.

1 As of 7/21/2021

2 Through 6/18/2021

3 https://www.investopedia.com/articles/economics/08/japan-1990s-credit-crunch-liquidity-trap.asp

4 https://www.macrotrends.net/2593/nikkei-225-index-historical-chart-data

5 As of 7/21/2021

*Guaranteed by an insurance carrier. Optional enhancement riders may be added to the policy for an additional charge. These are hypothetical average numbers based off of A+ rated carriers.

This material is not a recommendation to buy, sell, hold, or roll over any asset, adopt a financial strategy or use a particular account type. It does not take into account the specific investment objectives, tax and financial condition or particular needs of any specific person. You should work with your financial professional to discuss your specific situation. Guarantees are provided and backed by the financial strength of an insurance company. Optional enhancement riders may be added to the policy for an additional charge. Hypothetical average FIA numbers are based off of A+ rated carriers.