This is a picture of what we refer to as “Churn.” The 200-day moving average (DMA) is generally

considered to be a bullish indicator for the S&P 500 when the plot is above it, and a bearish indicator

when the plot is below it.

What we have witnessed this year is 5 movements higher and 6 movements below this year. So, it is

apparent that this is the classic “tussle” between bulls and bears. There is no shortage of concern from

higher interest rates, commodity prices that did not begin rising with the Russian invasion of

Ukraine…they began cycling higher over a year ago, to what the “crazy” Russians are doing, along with

the CCP (Chinese Communist Party) intends to do with its continued annexation of territory in the south

Pacific.

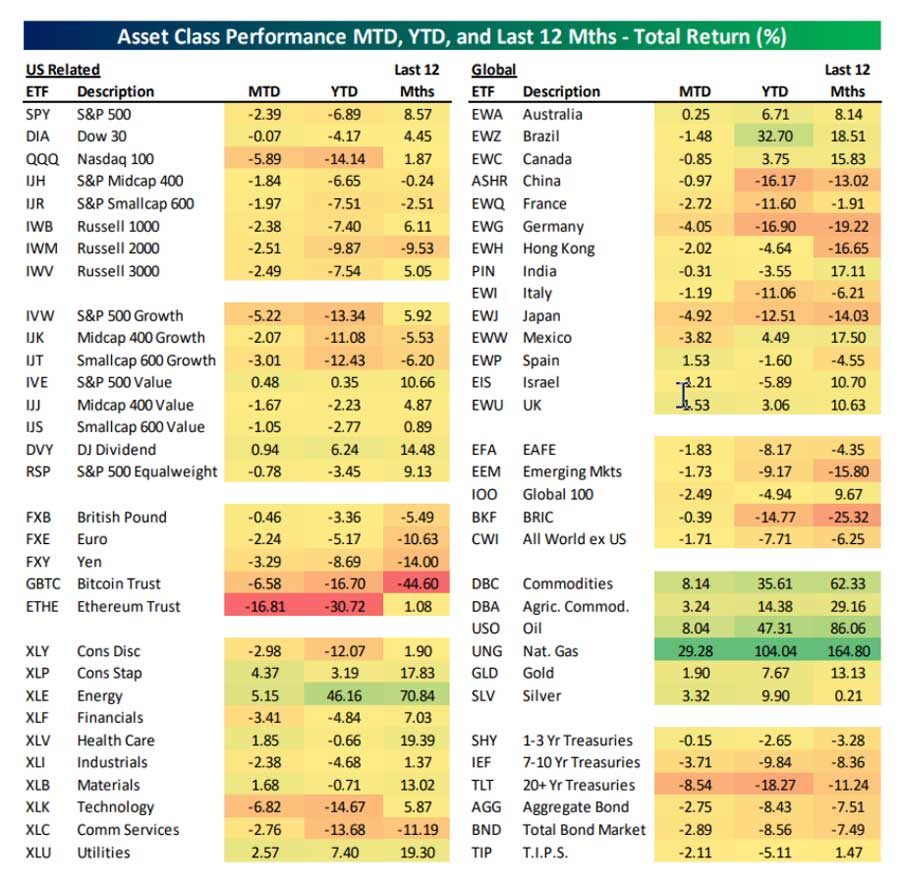

There have been some clear “winners and losers” over the past month, year-to-date, and over the past

12 months, as can be seen from the table below, courtesy of Bespoke.

Commodities have continued to post positive gains in asset classes while stocks and bonds have been under pressure for most of 2022. Within stocks, the strategies that worked well last year have reverted to the man a bit, with S&P Growth underperforming S&P Value over the past month and on a year-to-date basis.

Our portfolios have been oriented toward Growth, primarily because of our concentration in technology and healthcare stocks, with increasing allocations more recently to energy and financials. In spite of the first quarter weakness in these sectors, which we attribute to their higher levels of valuation, we are not moving too far from this original tilt for the following reasons:

- Technology company fundamentals, for the most part, are amongst the best balance sheets in the equity markets.

- Technology has been hampered by continuing issues (Covid zero tolerance policies and threat of war) in Asia, but we are witnessing companies like Foxconn and Taiwan Semiconductor add to their manufacturing capacity in the United States.

- Demand remains strong and technology is not a luxury. It is one of the best means by which companies today can secure a competitive edge.

While technology company stock prices have been volatile in the first quarter, we believe that they are like “new tennis balls” and will come bouncing back.

As you can see from the chart above, the so-called “safety in bonds” has been hard to find over the past 12, 4 and one-half month. With the Fed having the unenviable task of having to now fight the highest inflation in 40 years, coupled with the uncertainties of global embargos and warfare, and imbalances that are enormous, I think that bonds are going to be a difficult place to find much appreciation outside of the coupon (interest) income that they spin off. As a result of this we are investing in fewer bond funds and more individual bonds where we know that, in spite of fluctuating market values, we can predetermine the return of principal (subject to credit risk), the time to maturity or call, and the rate of return on the bond investment, through individual bond purchases.

Looking forward, we are less sanguine about the risk of inflation than our colleagues over at Goldman who today raised their odds of a recession by roughly 10 points to 35%. We believe that the risk is closer to 50% at this point, though we remain cognizant that the world is awash in money at the moment which may have the effect of prolonging the cycle further or muting the impact of a recessionary trend. In this environment, we are of the opinion that the days of relatively easy performance are about over. In this kind of environment, I have found, over the years, that we can generally provide very good performance through the ownership of individual stocks and bonds, as opposed to funds. There tends to be a bit less diversification, but we believe that the difference is alpha generated and usually outweighs the diversification benefits of using a fund. In a rising rate environment, which we have not enjoyed in over 30 years, individual bond ownership in my view, trumps the diversification benefits of funds because of the certainty of return that can be enjoyed.

For clients wanting protection of principal and either an accumulation strategy or an income strategy, higher interest rates benefit annuity returns, particularly fixed indexed annuities. As well some new annuity strategies address common retirement returns like a Social Security reduction in benefits, chronic illness, the need for long-term care, or simply establishing a legacy for your loved ones. The growth and development of innovative and lower priced annuity strategies for retirees and potential retirees is truly amazing over the past 12 months. As you know, we often recommend using this strategy to provide a portfolio with gamma…the generation of a lower portfolio risk level with higher long-term returns. If you would like to explore how this might fit into your portfolio, please call me. If you have a portfolio with us, you will notice some of these directional trends this month. If you do not have a portfolio with us but would like to learn more about our processes, please call either Mike Robinson, Tom Pollock, or myself and we would be more than happy to introduce you to the “Gamma Formula.”

We are, finally, hopeful that the war between Russia and Ukraine will end soon. Until it does, we believe that market volatility remains dangerously high and systemically exposed to further supply chain disruptions, acceleration of commodity prices, and the possibility of a sudden and dramatic escalation by the Russians. We hope not, but, because of this potential, we are more cautious and defensive, and we are maintaining higher than normal cash allocations.

Best Regards,

Curt Lyman

clyman@abgwealth.com